424B3: Prospectus filed pursuant to Rule 424(b)(3)

Published on February 26, 2021

Table of Contents

Filed Pursuant to Rule 424(b)(3)

Registration Statement No. 333-251552

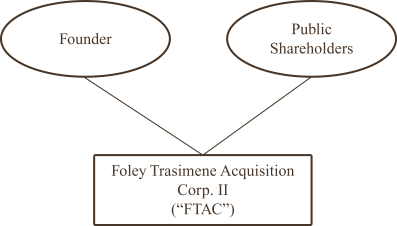

FOLEY TRASIMENE ACQUISITION CORP. II

1701 Village Center Circle,

Las Vegas, NV 89134

NOTICE OF SPECIAL MEETING OF STOCKHOLDERS

TO BE HELD ON MARCH 25, 2021

TO THE STOCKHOLDERS OF FOLEY TRASIMENE ACQUISITION CORP. II:

NOTICE IS HEREBY GIVEN that a special meeting of stockholders (the Special Meeting) of Foley Trasimene Acquisition Corp. II, a Delaware corporation (FTAC), will be held on March 25, 2021 at 12:00 p.m. Eastern Time. The Special Meeting will be a completely virtual meeting of stockholders, which will be conducted via live webcast. FTAC Stockholders will be able to attend the Special Meeting remotely, vote and submit questions during the Special Meeting by visiting https://www.cstproxy.com/foleytrasimene2/sm2021. We are pleased to utilize virtual stockholder meeting technology to (a) provide ready access and cost savings for FTACs stockholders and FTAC, and (b) to promote social distancing pursuant to guidance provided by the Centers for Disease Control and Prevention (CDC) and the U.S. Securities and Exchange Commission (SEC) due to the novel coronavirus (COVID-19). The virtual meeting format allows attendance from any location in the world. You are cordially invited to attend the Special Meeting, which will be held for the following purposes:

| (1) | Proposal No. 1To consider and vote upon a proposal to approve the Business Combination described in the accompanying proxy statement/prospectus, including (a) adopting the Agreement and Plan of Merger dated effective as of December 7, 2020 (the Merger Agreement) by and among FTAC, Paysafe Limited, an exempted limited company incorporated under the laws of Bermuda (Paysafe Limited), Paysafe Merger Sub Inc., a Delaware corporation and direct, wholly owned subsidiary of Paysafe Limited (Merger Sub), Paysafe Bermuda Holding LLC, a Bermuda exempted limited liability company (the LLC), Pi Jersey Holdco 1.5 Limited, a private limited company incorporated under the laws of Jersey, Channel Islands (the Accounting Predecessor), and Paysafe Group Holdings Limited, a private limited company incorporated under the laws of England and Wales (PGHL), and the transactions contemplated by the Merger Agreement (collectively, the Business Combination), pursuant to which, subject to the terms and conditions set forth therein, at the Closing, among other things, (i) Merger Sub will merge with and into FTAC, with FTAC being the surviving corporation in the merger and an indirect subsidiary of Paysafe Limited (Merger) and each outstanding share of FTAC Class A Common Stock and FTAC Class B Common Stock (other than certain excluded shares) will convert into the right to receive one common share, par value $0.001 per share, of Paysafe Limited (Company Common Shares), and (ii) PGHL will transfer and contribute the Accounting Predecessor to the Company in exchange for Company Common Shares and cash, (b) approving the issuance of shares of Class C common stock, par value $0.0001 of FTAC (Class C Common Stock), to Trasimene Capital FT, LP II, (the Founder) in exchange for the existing private placement warrants held by the Founder, pursuant to the requirements of Section 312.03(b) of the New York Stock Exchanges Listed Company Manual and (c) approving the other transactions contemplated by the Merger Agreement and related agreements described in the accompanying proxy statement/prospectuswe refer to this proposal as the Business Combination Proposal. A copy of the Merger Agreement is attached to this proxy statement/prospectus as Annex A. |

| (2) | Proposal No. 2To consider and vote upon a proposal to approve and adopt the third amended and restated certificate of incorporation of FTAC in the form attached hereto as Annex B (the Third Amended and Restated Certificate of Incorporation)we refer to this proposal as the Charter Amendment Proposal. |

| (3) | Proposal No. 3To consider and vote upon, on a non-binding advisory basis, certain governance provisions in the amended and restated bye-laws of Paysafe Limited (the Company Bye-laws), presented separately in accordance with the SEC requirementswe refer to this as the Governance Proposal. |

Table of Contents

| (4) | Proposal No. 4To consider and vote upon a proposal to approve and adopt the Paysafe Limited 2021 Omnibus Incentive Plan (the Omnibus Incentive Plan), which, among other things, provides for the reservation for issuance of a number of Company Common Shares as set forth in the Omnibus Incentive Plan, subject to annual increases as provided thereinwe refer to this as the Omnibus Incentive Plan Proposal. A copy of the Omnibus Incentive Plan is attached to this proxy statement/prospectus as Annex E. |

| (5) | Proposal No. 5To consider and vote upon a proposal to adjourn the Special Meeting to a later date or dates, if necessary, to permit further solicitation and vote of proxies in the event that there are insufficient votes for, or otherwise in connection with, the approval of the Business Combination Proposal, the Charter Amendment Proposal, the Governance Proposal or the Omnibus Incentive Plan Proposal. We refer to this proposal as the Adjournment Proposal and, together with the Business Combination Proposal, the Governance Proposal, the Charter Amendment Proposal and the Omnibus Incentive Plan Proposal as the Proposals. |

These Proposals are described in the accompanying proxy statement/prospectus, which we encourage you to read in its entirety before voting. Only holders of record of FTACs Class A common stock, par value $0.0001 per share (FTAC Class A Common Stock), and FTACs Class B common stock, par value $0.0001 per share (FTAC Class B Common Stock) at the close of business on February 17, 2021 (the Record Date) are entitled to notice of the Special Meeting and to vote and have their votes counted at the Special Meeting and any adjournments or postponements thereof.

After careful consideration, the FTAC Board has determined that the Business Combination Proposal, the Charter Amendment Proposal, the Governance Proposal, the Omnibus Incentive Plan Proposal and the Adjournment Proposal are fair to and in the best interests of FTAC and its stockholders and recommends voting FOR the Business Combination Proposal, FOR the Charter Amendment Proposal, FOR the Governance Proposal, FOR the Omnibus Incentive Plan Proposal and, if presented, FOR the Adjournment Proposal. See Proposal No. 1The Business CombinationFTACs Board of Directors Reasons for Approval of the Business Combination for additional information. Consummation of the Transactions are conditioned on the approval of each of the Business Combination Proposal and the Charter Amendment Proposal. If either of those proposals are not approved, we will not consummate the Transaction.

All stockholders of FTAC are cordially invited to attend the Special Meeting virtually. To ensure your representation at the Special Meeting, however, you are urged to mark, sign and date the enclosed proxy card and return it as soon as possible in the pre-addressed postage paid envelope provided. If you are a stockholder of record of FTAC Common Stock, you may also cast your vote by means of remote communication at the Special Meeting by navigating to https://www.cstproxy.com/foleytrasimene2/sm2021. If your shares are held in an account at a brokerage firm or bank, or by a nominee, you must instruct your broker, bank or nominee on how to vote your shares or, if you wish to attend the Special Meeting by means of remote communication you must obtain a proxy from your broker or bank. If the Business Combination Proposal or the Charter Amendment Proposal fails to receive the required approval by the stockholders of FTAC at the Special Meeting, the Business Combination will not be completed.

Whether or not you plan to attend the Special Meeting, we urge you to read the accompanying proxy statement/prospectus (and any documents incorporated into the accompanying proxy statement/prospectus by reference) carefully. Please pay particular attention to the section entitled Risk Factors beginning on page 47 in the accompanying proxy statement/prospectus.

Your vote is important regardless of the number of shares you own. Whether you plan to attend the Special Meeting or not, please mark, sign and date the enclosed proxy card and return it as soon as possible in the envelope provided. If your shares are held in street name or are in a margin or similar account, you should contact your broker to ensure that votes related to the shares you beneficially own are properly counted.

Table of Contents

Thank you for your participation. We look forward to your continued support.

| By Order of the Board of Directors | ||

|

|

||

| William P. Foley, II | ||

| Chairman of the Board of Directors | ||

February 26, 2021

IF YOU RETURN YOUR PROXY CARD WITHOUT AN INDICATION OF HOW YOU WISH TO VOTE, YOUR SHARES WILL BE VOTED FOR EACH OF THE PROPOSALS.

YOU MAY EXERCISE YOUR RIGHTS TO DEMAND THAT FTAC REDEEM YOUR SHARES FOR A PRO RATA PORTION OF THE FUNDS HELD IN THE TRUST ACCOUNT WHETHER YOU VOTE FOR OR AGAINST THE PROPOSALS OR DO NOT VOTE ON THE PROPOSALS AND WHETHER OR NOT YOU ARE HOLDER OF SHARES AS OF THE RECORD DATE OR ACQUIRED YOUR SHARES AFTER THE RECORD DATE. TO EXERCISE YOUR REDEMPTION RIGHTS, YOU MUST TENDER YOUR SHARES TO FTACS TRANSFER AGENT AT LEAST TWO (2) BUSINESS DAYS PRIOR TO THE SPECIAL MEETING. YOU MAY TENDER YOUR SHARES FOR REDEMPTION BY EITHER DELIVERING YOUR SHARE CERTIFICATE TO THE TRANSFER AGENT OR BY DELIVERING YOUR SHARES ELECTRONICALLY USING THE DEPOSITORY TRUST COMPANYS DEPOSIT/WITHDRAWAL AT CUSTODIAN (DWAC) SYSTEM. IF THE BUSINESS COMBINATION IS NOT COMPLETED, THEN THESE TENDERED SHARES WILL NOT BE REDEEMED FOR CASH AND WILL BE RETURNED TO THE APPLICABLE STOCKHOLDER. IF YOU HOLD THE SHARES IN STREET NAME, YOU WILL NEED TO INSTRUCT THE ACCOUNT EXECUTIVE AT YOUR BROKER OR BANK TO WITHDRAW THE SHARES FROM YOUR ACCOUNT IN ORDER TO EXERCISE YOUR REDEMPTION RIGHTS. SEE THE SECTION ENTITLED SPECIAL MEETING OF FTAC STOCKHOLDERSREDEMPTION RIGHTS FOR MORE SPECIFIC INSTRUCTIONS.

Table of Contents

PROXY STATEMENT FOR SPECIAL MEETING OF STOCKHOLDERS OF

FOLEY TRASIMENE ACQUISITION CORP. II

and

PROSPECTUS FOR UP TO 146,703,345 COMMON SHARES, 48,901,115 WARRANTS AND 48,901,115

COMMON SHARES ISSUABLE UPON EXERCISE OF WARRANTS

OF

PAYSAFE LIMITED

Dear Foley Trasimene Acquisition Corp. II Stockholders,

On behalf of the FTAC board of directors, which we refer to as the FTAC Board, we cordially invite you to a special meeting, which we refer to as the Special Meeting, of stockholders of Foley Trasimene Acquisition Corp. II, a Delaware corporation, which we refer to as FTAC, to be held via live webcast at 12:00 p.m. Eastern Time, on March 25, 2021. The Special Meeting can be accessed by visiting https://www.cstproxy.com/foleytrasimene2/sm2021, where you will be able to listen to the meeting live and vote during the meeting. Please note that you will only be able to access the special meeting by means of remote communication.

This proxy statement/prospectus is being provided to the stockholders of FTAC, in connection with the proposed business combination with Paysafe Group Holdings Limited, a private limited company incorporated under the laws of England and Wales, which we refer to as PGHL, and Paysafe Limited, an exempted limited company incorporated under the laws of Bermuda, which we refer to as the Company. These terms and others used in this introduction are defined in greater detail below in this proxy statement/prospectus under the caption Frequently Used Terms.

Pursuant to the Agreement and Plan of Merger, dated as of December 7, 2020, by and among FTAC, the Company, Paysafe Merger Sub Inc., a Delaware corporation and direct, wholly owned subsidiary of the Company, which we refer to as Merger Sub, Paysafe Bermuda Holding LLC, a Bermuda exempted limited liability company, which we refer to as the LLC, Pi Jersey Holdco 1.5 Limited, a private limited company incorporated under the laws of Jersey, Channel Islands, which we refer to as the Accounting Predecessor, and PGHL, which we refer to as the Merger Agreement, among other things, (i) Merger Sub will merge with and into FTAC, with FTAC being the surviving corporation in the merger and an indirect subsidiary of the Company, which we refer to as the Merger and each outstanding share of common stock of FTAC (other than certain excluded shares) will convert into the right to receive one common share, par value $0.001 per share, of the Company, which we refer to as Company Common Shares, and (ii) PGHL will transfer and contribute the Accounting Predecessor to the Company in exchange for Company Common Shares and cash, which we refer to as the Paysafe Contribution. We refer to the transactions contemplated by the Merger Agreement as the Business Combination.

The consideration to be paid to PGHL will be paid in a combination of stock and cash consideration, which we refer to as the Closing Transaction Consideration. The cash consideration will be an amount equal to (i) (x) all amounts in FTACs trust account (after reduction for the aggregate amount of payments required to be made in connection with any valid stockholder redemptions), plus (y) the aggregate amount of cash that has been funded pursuant to the Subscription Agreements (as defined below) as of immediately prior to the closing, plus (z) the aggregate amount of cash that has been funded pursuant to that certain Forward Purchase Agreement, by and between FTAC and Cannae Holdings, dated as of August 18, 2020, as of immediately prior to the closing, we refer to such amounts in clauses (x), (y) and (z) as the Available Cash Amount, minus (ii) any excess amount of the Companys net debt over $1,805,000,000, minus (iii) any transaction expenses, which amount we refer to as the Closing Cash Consideration. The remainder of the Closing Transaction Consideration will be paid in a number of Company Common Shares equal to (A) (i) $8,713,000,000, minus (ii) the Companys net

Table of Contents

debt, minus (iii) any transaction expenses, plus (iv) the aggregate price of permitted acquisitions, if any, minus (v) Closing Cash Consideration, divided by (B) $10.00 per share, which amount we refer to as the Closing Seller Shares.

At the effective time of the Merger, each share of FTACs Class A common stock, par value $0.0001 per share, which we refer to as the FTAC Class A Common Stock, and FTACs Class B common stock, par value $0.0001 per share, which we refer to as the FTAC Class B Common Stock will be cancelled and automatically deemed for all purposes to represent the right to receive, in the aggregate, one Company Common Share. At the effective time of the Merger, each of FTACs public warrants that are outstanding immediately prior to the effective time will, pursuant to and in accordance with the warrant agreement covering such warrants, automatically and irrevocably be modified to provide that such warrant will no longer entitle the holder thereof to purchase the amount of share(s) of FTAC common stock set forth therein and in substitution thereof such warrant will entitle the holder thereof to acquire the same number of Company Common Shares per warrant on the same terms.

In connection with the consummation of the Business Combination and immediately prior thereto, the warrants held by Trasimene Capital FT, LP II, which we refer to as FTAC Founder or the Founder will be exchanged for shares of Class C Common Stock, par value $0.0001 of FTAC, which we refer to as Class C Common Stock, and immediately thereafter the Founder will transfer and contribute such shares of Class C Common Stock to the LLC in exchange for exchangeable units of the LLC (as provided for in the Sponsor Agreement described herein). Such exchangeable units will be exchangeable into Company Common Shares or cash, as determined by the LLC, on the same terms as such warrants, following the first anniversary of the closing and expiring on the fifth anniversary of the closing.

At the Special Meeting, FTAC Stockholders will be asked to consider and vote upon:

(1) Proposal No. 1 To consider and vote upon a proposal to approve the Business Combination described in the accompanying proxy statement/prospectus, including (a) adopting the Merger Agreement, (b) the issuance of the Class C Common Stock in exchange for the warrants held by the FTAC Founder and (c) approving the other transactions contemplated by the Merger Agreement and related agreements described in the accompanying proxy statement/prospectuswe refer to this proposal as the Business Combination Proposal;

(2) Proposal No. 2 To consider and vote upon a proposal to approve and adopt the third amended and restated certificate of incorporation of FTAC in the form attached hereto as Annex B, which we refer to as the Third Amended and Restated Certificate of Incorporationwe refer to this proposal as the Charter Amendment Proposal;

(3) Proposal No. 3To consider and vote upon, on a non-binding advisory basis, certain governance provisions in the Company Bye-laws, presented separately in accordance with the SEC requirementswe refer to this as the Governance Proposal;

(4) Proposal No. 4To consider and vote on a proposal to approve and adopt the Paysafe Limited 2021 Omnibus Incentive Plan, which we refer to as the Omnibus Incentive Plan and the material terms thereunder, including the authorization of the initial share reserve thereunderwe refer to this proposal as the Omnibus Incentive Plan Proposal. A copy of the Omnibus Incentive Plan is attached to the accompanying proxy statement/prospectus as Annex E; and

(5) Proposal No. 5To consider and vote upon a proposal to adjourn the Special Meeting to a later date or dates, if necessary, to permit further solicitation and vote of proxies in the event that there are insufficient votes for, or otherwise in connection with, the approval of the Business Combination Proposal, the Charter Amendment Proposal, the Governance Proposal or the Omnibus Incentive Plan Proposalwe refer to this proposal as the Adjournment Proposal.

Each of these proposals is more fully described in the accompanying proxy statement/prospectus, which we encourage you to read carefully and in its entirety before voting. Only holders of record of FTAC Class A Common Stock and FTAC Class B Common Stock at the close of business on February 17, 2021 are entitled to notice of the Special Meeting and to vote and have their votes counted at the Special Meeting and any adjournments or postponements thereof.

Table of Contents

After careful consideration, the FTAC Board has determined that the Business Combination Proposal, the Charter Amendment Proposal, the Governance Proposal, the Omnibus Incentive Plan Proposal and the Adjournment Proposal are fair to and in the best interests of FTAC and its stockholders and recommends voting FOR the Business Combination Proposal, FOR the Charter Amendment Proposal, FOR the Governance Proposal, FOR the Omnibus Incentive Plan Proposal and, if presented, FOR the Adjournment Proposal. See Proposal No. 1 The Business Combination FTACs Board of Directors Reasons for Approval of the Business Combination for additional information. Consummation of the Transactions is conditioned on the approval of each of the Business Combination Proposal and the Charter Amendment Proposal. If either of those proposals are not approved, we will not consummate the Transaction.

The Merger Agreement is attached to this proxy statement/prospectus as Annex A. The Company Charter is attached to this proxy statement/prospectus as Annex C and the Company Bye-laws will be amended and restated substantially in the form attached to this proxy statement/prospectus as Annex D.

On July 31, 2020, FTAC entered into a Forward Purchase Agreement with Cannae Holdings, Inc., which we refer to as Cannae Holdings, pursuant to which Cannae Holdings agreed to purchase an aggregate of 15,000,000 shares of FTAC Class A Common Stock, plus an aggregate of 5,000,000 redeemable warrants to purchase shares of FTAC Class A Common Stock at $11.50 per unit, for an aggregate purchase price of $150,000,000, or $10.00 for one share of FTAC Class A Common Stock and one-third of one private placement warrant, in a private placement to occur concurrently with the closing of the Business Combination. Each share of FTAC Class A Common Stock held by Cannae Holdings as of the closing will become one Company Common Share. Each of the warrants held by Cannae Holdings as of the closing will become one warrant to acquire a Company Common Share.

Concurrently with the execution and delivery of the Merger Agreement, the Company, FTAC and certain investors (including a subsidiary of Cannae Holdings), referred to collectively as the PIPE Investors, entered into Subscription Agreements, pursuant to which the PIPE Investors have committed to purchase, concurrently with the closing of the Business Combination, in the aggregate, 200 million Company Common Shares for $10.00 per share or an aggregate purchase price equal to $2.0 billion.

All FTAC Stockholders are cordially invited to attend the special meeting and we are providing the accompanying proxy statement/prospectus and proxy card in connection with the solicitation of proxies to be voted at the Special Meeting (or any adjournment or postponement thereof). To ensure your representation at the Special Meeting, however, you are urged to complete, sign, date and return the enclosed proxy card as soon as possible. If your shares are held in an account at a brokerage firm or bank, you must instruct your broker or bank on how to vote your shares or, if you wish to attend the Special Meeting and vote, obtain a proxy from your broker or bank.

FTACs Units (each consisting of one share of FTAC Class A Common Stock and one-third of one warrant to acquire a share of FTAC Class A Common Stock, which we refer to as a FTAC Warrant), FTAC Class A Common Stock and FTAC Warrants are currently listed on the New York Stock Exchange, which we refer to as the NYSE, under the symbols BFT.U, BFT and BFT.WS, respectively. The Company will apply for listing, effective upon the closing of the Business Combination, of its common shares and warrants on the NYSE, under the symbols PSFE and PSFE.WS, respectively.

Pursuant to the FTAC Charter, in connection with the completion of the Business Combination, holders of shares of FTAC Class A Common Stock may elect to have their shares redeemed for cash from FTACs trust account at the applicable redemption price per share calculated in accordance with the FTAC Charter. Payment for such redemptions will come from FTACs trust account that holds a portion of the proceeds of FTACs initial public offering and the concurrent sale of its private placement Units. To the extent holders of shares of FTAC Class A Common Stock elect to have their shares redeemed, the Closing Cash Consideration and the Closing Seller Shares to be paid to PGHL will vary, as described herein.

Table of Contents

Proposals to approve the Merger Agreement and the other matters discussed in this proxy statement/prospectus will be presented at the Special Meeting of stockholders of FTAC scheduled to be held on March 25, 2021.

This proxy statement/prospectus provides you with detailed information about the Business Combination and other matters to be considered at the Special Meeting of FTACs stockholders. We encourage you to carefully read this entire document. You should also carefully consider the risk factors described in Risk Factors beginning on page 47.

Your vote is important regardless of the number of shares you own. Whether you plan to attend the Special Meeting or not, please sign, date and return the enclosed proxy card as soon as possible in the envelope provided. If your shares are held in street name or are in a margin or similar account, you should contact your broker to ensure that votes related to the shares you beneficially own are properly counted.

The transactions described in the accompanying proxy statement/prospectus have not been approved or disapproved by the Securities and Exchange Commission or any state securities commission nor has the Securities and Exchange Commission or any state securities commission passed upon the accuracy or adequacy of this proxy statement/prospectus. Any representation to the contrary is a criminal offense.

Thank you for your participation. We look forward to your continued support.

| By Order of the Board of Directors | ||

|

|

||

| William P. Foley, II Chairman of the Board of Directors |

||

IF YOU RETURN YOUR PROXY CARD WITHOUT AN INDICATION OF HOW YOU WISH TO VOTE, YOUR SHARES WILL BE VOTED IN FAVOR OF EACH OF THE PROPOSALS.

TO EXERCISE YOUR REDEMPTION RIGHTS, YOU MUST ELECT TO HAVE FTAC REDEEM YOUR SHARES FOR A PRO RATA PORTION OF THE FUNDS HELD IN THE TRUST ACCOUNT AND TENDER YOUR SHARES TO FTACS TRANSFER AGENT AT LEAST TWO (2) BUSINESS DAYS PRIOR TO THE VOTE AT THE SPECIAL MEETING. YOU MAY TENDER YOUR SHARES BY EITHER DELIVERING YOUR SHARE CERTIFICATE TO THE TRANSFER AGENT OR BY DELIVERING YOUR SHARES ELECTRONICALLY USING THE DEPOSITORY TRUST COMPANYS DWAC (DEPOSIT AND WITHDRAWAL AT CUSTODIAN) SYSTEM. IF THE BUSINESS COMBINATION IS NOT COMPLETED, THEN THESE SHARES WILL NOT BE REDEEMED FOR CASH. IF YOU HOLD THE SHARES IN STREET NAME, YOU WILL NEED TO INSTRUCT THE ACCOUNT EXECUTIVE AT YOUR BANK OR BROKER TO WITHDRAW THE SHARES FROM YOUR ACCOUNT IN ORDER TO EXERCISE YOUR REDEMPTION RIGHTS. PLEASE SEE THE SECTION ENTITLED SPECIAL MEETING OF FTAC STOCKHOLDERS REDEMPTION RIGHTS FOR MORE SPECIFIC INSTRUCTIONS.

This proxy statement/prospectus is dated February 26, 2021, and is first being mailed to FTACs stockholders on or about March 1, 2021.

Table of Contents

| Page | ||||

| 1 | ||||

| 1 | ||||

| 1 | ||||

| 3 | ||||

| 13 | ||||

| 26 | ||||

| SUMMARY UNAUDITED PRO FORMA CONDENSED COMBINED FINANCIAL INFORMATION |

43 | |||

| 45 | ||||

| 47 | ||||

| 106 | ||||

| 108 | ||||

| 113 | ||||

| 162 | ||||

| 164 | ||||

| 167 | ||||

| 174 | ||||

| UNAUDITED PRO FORMA CONDENSED COMBINED FINANCIAL INFORMATION |

175 | |||

| 189 | ||||

| FTACS MANAGEMENTS DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATION |

197 | |||

| 201 | ||||

| PAYSAFES MANAGEMENTS DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATION |

240 | |||

| 275 | ||||

| 285 | ||||

| 288 | ||||

| 297 | ||||

| 308 | ||||

| 314 | ||||

| 327 | ||||

| 327 | ||||

| 327 | ||||

| 328 | ||||

| 328 | ||||

| 329 | ||||

| 329 | ||||

| 329 | ||||

| 329 | ||||

| 329 | ||||

| F-1 | ||||

ANNEXES

Annex A: Agreement and Plan of Merger

Annex B: Third Amended and Restated Certificate of Incorporation of FTAC

Annex C: Memorandum of Association of Paysafe Limited

Annex D: Form of Amended and Restated Bye-laws of Paysafe Limited

Annex E: The Omnibus Incentive Plan

i

Table of Contents

ABOUT THIS PROXY STATEMENT/PROSPECTUS

This document, which forms part of a registration statement on Form F-4 filed with the U.S. Securities and Exchange Commission, or the SEC, by the Company, constitutes a prospectus of the Company under Section 5 of the U.S. Securities Act of 1933, as amended, or the Securities Act, with respect to the Company Common Shares to be issued to FTAC Stockholders, the Company Warrants to be issued to warrant holders and the Company Common Shares underlying such warrants, if the Business Combination described herein is consummated. This document also constitutes a notice of meeting and a proxy statement under Section 14(a) of the U.S. Securities Exchange Act of 1934, as amended, or the Exchange Act, with respect to the Special Meeting of FTAC Stockholders at which FTAC Stockholders will be asked to consider and vote upon a proposal to approve the Business Combination by the adoption of the Merger Agreement, among other matters.

FINANCIAL STATEMENT PRESENTATION

Paysafe Limited

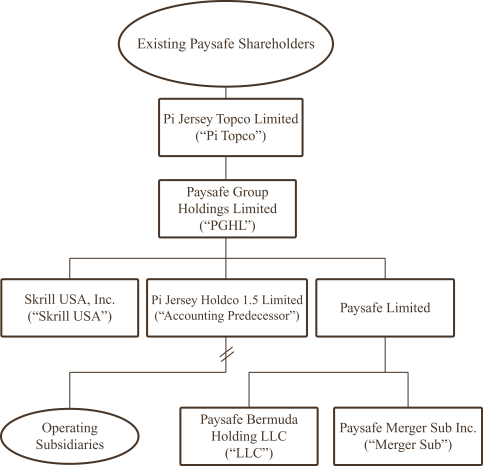

Paysafe Limited was incorporated by PGHL under the laws of Bermuda on November 23, 2020 for the purpose of effectuating the Business Combination described herein. Paysafe Limited has no material assets and does not operate any businesses. Accordingly, no financial statements have been included in this proxy statement/prospectus. The Business Combination will result in Paysafe Limited acquiring, and becoming the successor to, the Accounting Predecessor. Simultaneously, it will complete the combination with the public shell company, FTAC, with an exchange of the shares and warrants issued by Paysafe Limited for those of FTAC. The Business Combination will be accounted for as a capital reorganization followed by the combination with FTAC, which will be treated as a recapitalization. Following the Business Combination, both the Accounting Predecessor and FTAC will be indirect wholly owned subsidiaries of Paysafe Limited.

The Accounting Predecessor

As a result of the transaction being accounted for as a capital reorganization, Pi Jersey Holdco 1.5 Limited will be deemed to be the Accounting Predecessor of Paysafe Limited. The Accounting Predecessor has a direct voting interest or a variable interest in the Groups activities and operations that result in revenues, expenses, assets and liabilities.

The financial statements for the Accounting Predecessor are included in this proxy statement/prospectus for the year ended December 31, 2019, and comparative period for the year ended December 31, 2018 (the Paysafe Audited 2019 Consolidated Financial Statements) along with unaudited condensed consolidated interim results for the nine months ended September 30, 2020, and comparative period for the nine months ended September 30, 2019 (the Paysafe Unaudited 2020 Interim Condensed Consolidated Financial Statements and, together with the Paysafe Audited 2019 Consolidated Financial Statements, the Paysafe Consolidated Financial Statements).

In this proxy statement/prospectus, we present industry data, forecasts, information and statistics regarding the markets in which we compete as well as our analysis of statistics, data and other information that we have derived from third parties, including independent consultant reports, publicly available information, various industry publications and other published industry sources (including Mastercards investor presentation, eMarketer Inc.s global eCommerce report dated June 2020 (referred to herein as eMarketer), the Strawhecker Group, Nilson, FIS, Newzoo, Eilers & Krejcik, H2 Gambling Capital, Allied Market Research,Glenbrook and Boston Consulting Group). Independent consultant reports, industry publications and other published industry sources generally indicate that the information contained therein was obtained from sources believed to be

1

Table of Contents

reliable. Such information is supplemented where necessary with our own internal estimates and information obtained from discussions with our customers, taking into account publicly available information about other industry participants and our managements judgment where information is not publicly available. This information appears in Summary of the Proxy Statement/Prospectus, Information Related to Paysafe, Paysafes Managements Discussion and Analysis of Financial Condition and Results of Operation and other sections of this proxy statement/prospectus.

Although we believe that these third-party sources are reliable, it does not guarantee the accuracy or completeness of this information, and we have not independently verified this information. Forecasts and other forward-looking information obtained from these sources are subject to the same qualifications and uncertainties as the other forward-looking statements in this proxy statement/prospectus. These forecasts and forward-looking information are subject to uncertainty and risk due to a variety of factors, including those described under Risk Factors. These and other factors could cause results to differ materially from those expressed in any forecasts or estimates. Some market data and statistical information are also based on our good faith estimates, which are derived from managements knowledge of our industry and such independent sources referred to above. Certain market, ranking and industry data included elsewhere in this proxy statement/prospectus, including the size of certain markets and our size or position and the positions of our competitors within these markets, including its services relative to its competitors, are based on estimates by us. These estimates have been derived from managements knowledge and experience in the markets in which we operate, as well as information obtained from surveys, reports by market research firms, our customers, distributors, suppliers, trade and business organizations and other contacts in the markets in which we operate and have not been verified by independent sources. Unless otherwise noted, all of our market share and market position information presented in this proxy statement/prospectus is an approximation. Our market share and market position in each of our business segments, unless otherwise noted, is based on our volume relative to the estimated volume in the markets served by each of our business segments. References herein to Paysafe being a leader in a market or product category refer to our belief that we have a leading market share position in each specified market, unless the context otherwise requires. As there are no publicly available sources supporting this belief, it is based solely on our internal analysis of our volume as compared to the estimated volume of our competitors. In addition, the discussion herein regarding our various end markets is based on how it defines the end markets for its products, which products may be either part of larger overall end markets or end markets that include other types of products and services.

Our internal data and estimates are based upon information obtained from trade and business organizations and other contacts in the markets in which we operate and managements understanding of industry conditions. Although we believe that such information is reliable, it has not had this information verified by any independent sources.

2

Table of Contents

Unless otherwise stated or unless the context otherwise requires, all references to we, us, our, Paysafe or the Company refer to (i) Pi Jersey Holdco 1.5 Limited prior to the consummation of the Business Combination and to (ii) Paysafe Limited following the consummation of the Business Combination.

In addition, in this document:

Absolute Share Limit means total number of Company Common Shares that may be issued under the Omnibus Incentive Plan.

Accounting Predecessor means Pi Jersey Holdco 1.5 Limited, a private limited company incorporated under the laws of Jersey, Channel Islands.

Additional I/C Loans means FTACs loans out of the Available Cash Amount, caused by the Company, to certain Subsidiaries of the Company following the FTAC Contribution.

Adjournment Proposal means the proposal to adjourn the Special Meeting of the stockholders of FTAC to a later date or dates, if necessary, to permit further solicitation and vote of proxies if, based upon the tabulated vote at the time of the Special Meeting, there are not sufficient votes to approve the Business Combination Proposal.

Affiliate means, with respect to any specified Person, any Person that, directly or indirectly, controls, is controlled by, or is under common control with, such specified Person, through one or more intermediaries or otherwise; provided, except for the Company and its Subsidiaries, no Affiliate or portfolio company (as such term is commonly understood in the private equity industry) of funds advised by affiliates of CVC or Blackstone or any of their respective Affiliates shall be considered an Affiliate of the Company or any of its Subsidiaries.

Aggregate Permitted Acquisition Price Amount means, without duplication, the aggregate amount of consideration paid by any Paysafe Party prior to Closing in respect of all Permitted Acquisitions.

Antitrust Laws means the HSR Act, the Federal Trade Commission Act, as amended, the Sherman Act, as amended, the Clayton Act, as amended, and any applicable foreign antitrust Laws and all other applicable Laws that are designed or intended to prohibit, restrict or regulate actions having the purpose or effect of monopolization or restraint of trade or lessening of competition through merger or acquisition.

Available Cash Amount means, as of immediately prior to Closing, all available Cash and Cash Equivalents of FTAC and its Subsidiaries, including (i) all amounts in the Trust Account (after reduction for the aggregate amount of payments required to be made in connection with FTAC Stockholder Redemption), (ii) the PIPE Investment Proceeds, and (iii) the aggregate amount of cash proceeds from the FTAC Financing.

Blackstone means The Blackstone Group Inc.

Blackstone Investors means certain funds affiliated with Blackstone.

Brexit means the United Kingdom (UK) leaving the EU.

Broker Non-Vote means the failure of an FTAC stockholder, who holds his or her shares in street name through a broker or other nominee, to give voting instructions to such broker or other nominee.

Business Combination means the transactions contemplated by the Merger Agreement.

Business Combination Proposal means the proposal to adopt the Merger Agreement and approve the transactions contemplated thereby.

3

Table of Contents

CAGR means compounded annual growth rate.

Cannae means Cannae Holdings and Cannae LLC.

Cannae Holdings means Cannae Holdings, Inc.

Cannae LLC means Cannae Holdings LLC, a wholly-owned subsidiary of Cannae Holdings.

Cash and Cash Equivalents means, for any Person, all cash and cash equivalents (including marketable securities, checks and bank deposits); provided, however that with respect to PGHL and its Subsidiaries, such amount shall (x) exclude segregated account funds and liquid assets as more fully described on Exhibit F-1 attached to the Merger Agreement and (y) include any costs, fees and expenses associated with refinancing or repricing the existing indebtedness of the Company (in accordance with the Merger Agreement) that have not been paid on or prior to the Closing Date.

CBI means the Central Bank of Ireland.

CBI Approval means each required approval from the CBI of (i) the applicable Sponsor Persons and (ii) the Company and the LLC, pursuant to Regulation 44 of the European Communities (Electronic Money) Regulations 2011 (S.I. No. 183/2011) (as amended) and the requirements of the CBI, as a result of the transactions contemplated hereby, to the extent required by applicable Law.

Charter Amendment Proposal means the proposal to approve the amendment and restatement of the FTAC Charter.

Closing means the closing of the transactions contemplated by the Merger Agreement and the PIPE Investment agreements.

Closing Cash Consideration means an amount equal to the sum of (i) the Available Cash Amount, minus (ii) the Debt Repayment Amount, minus (iii) the Transaction Expenses.

Closing Date means the date on which the Closing is completed.

Closing Seller Shares means the number of Company Common Shares (rounded up to the nearest whole share) equal to (i) the Closing Seller Share Consideration, divided by (ii) $10.00.

Closing Transaction Consideration means an amount equal to (i) $8,713,000,000, minus (ii) Company Net Debt Amount, minus (iii) Transaction Expenses, plus (iv) the Aggregate Permitted Acquisition Price Amount, if any.

Code means the U.S. Internal Revenue Code of 1986, as amended.

Committee means the compensation committee of the Companys Board, or such other committee of the Companys Board to which it has properly delegated power, or if no such committee or subcommittee exists, the Companys Board which the Omnibus Incentive Plan will be administered by.

Company Board means the board of directors of the Company from time to time.

Company Bye-laws means the bye-laws of the Company to be amended and restated substantially in the form of Exhibit B attached to the Merger Agreement prior to the Effective Time.

Company Charter means the memorandum of association of the Company as in effect on the date hereof and substantially in the form of Exhibit A attached to the Merger Agreement.

4

Table of Contents

Company Common Share(s) means the common shares, par value $0.001 per share, of Paysafe Limited and any successors thereto or other classes of common share of the Company created in any Pre-Closing Recapitalization.

Company Net Debt Amount means, as of immediately prior to the Closing, an amount equal to (i) the aggregate indebtedness for borrowed money of PGHL and its Subsidiaries and indebtedness issued by PGHL and its Subsidiaries in substitution or exchange for borrowed money, excluding any items set forth on Exhibit F-1 attached to the Merger Agreement minus (ii) Cash and Cash Equivalents of PGHL and its Subsidiaries minus (iii) any costs, fees and expenses associated with refinancing or repricing the existing indebtedness of the Company (in accordance with the Merger Agreement) that have been paid on or prior to the Closing Date. An illustrative example of the Company Net Debt Amount is set forth on Exhibit F-2 attached to the Merger Agreement.

Company LLC Contribution means the transfer and contribution of FTAC and the Accounting Predecessor by the Company to the LLC in exchange for LLC Interests immediately following the I/C Loan.

Company Warrants means warrants that will entitle the holder thereof to purchase for $11.50 per share one Company Common Share in lieu of one share of FTAC Class A Common Stock (subject to adjustment in accordance with the Warrant Agreement).

COVID-19 means SARS-CoV-2 or COVID-19, and any evolutions thereof or any other epidemics, pandemics or disease outbreaks.

CVC means CVC Advisers Limited.

CVC Investors means Pi Holdings Jersey Limited and Pi Syndication LP.

CVC Party means Pi Holdings Jersey Limited.

Debt Repayment Amount means an amount equal to the excess, if any, of (i) the Company Net Debt Amount over (ii) the Specified Net Debt Amount.

DGCL means the Delaware General Corporation Law.

Effective Time has the meaning specified in Section 2.04 of the Merger Agreement.

ERISA means Employee Retirement Income Security Act of 1974.

EU means European Union.

EUR means Euro, the legal currency of the European Union.

Executive Management means members of the executive management of Paysafe.

Existing Paysafe Shareholders means CVC Investors, Blackstone Investors and Executive Management.

FCA means the UK Financial Conduct Authority and any successor authority thereto.

FCA Approval means each required prior approval from the FCA to, in accordance with s178 of the Financial Services and Markets Act 2000 (as amended from time to time) (FSMA), and the requirements of the FCA, any of (i) the applicable Sponsor Persons and (ii) the Company and the LLC for the purposes of the Part XII of FSMA as a result of the transactions contemplated hereby, to the extent required by applicable Law.

FNF Subscribers means each of Fidelity National Title Insurance Company, Commonwealth Land Title Insurance Company, Chicago Title Insurance Company and Fidelity & Guaranty Life Insurance Company, collectively, the FNF Subscribers.

5

Table of Contents

Forward Purchase Agreement means the forward purchase agreement, dated as of July 31, 2020, between FTAC and Cannae Holdings, Inc.

Founder means Trasimene Capital FT, LP II.

Founder FTAC Warrant Recapitalization means the recapitalization of the Private Placement Warrants for FTAC Class C Common Stock, consummated prior to the consummation of the Founder LLC Contribution, the Merger, the I/C Loan, the Company LLC Contribution, the FTAC Contribution and the Additional I/C Loans.

Founder LLC Contribution means the contribution by Founder of FTAC Class C Common Stock to the LLC in exchange for exchangeable units.

Founder Shares means the shares of FTAC Class B Common Stock held by the Founder.

FTAC means Foley Trasimene Acquisition Corp. II.

FTAC Affiliate Agreement means that FTAC is a party to any transaction, agreement, arrangement or understanding with any (i) present or former equityholder, executive officer or director of FTAC, (ii) beneficial owner (within the meaning of Section 13(d) of the Exchange Act) of 5% or more of the capital stock or equity interests of any of the Company or its Subsidiaries or (iii) Affiliate, associate or member of the immediate family (as such terms are respectively defined in Rules 12b-2 and 16a-1 of the Exchange Act).

FTAC Benefit Plan means any employee benefit plan as defined in Section 3(3) of ERISA (including Multiemployer Plans), or any stock purchase, stock option, severance, employment, individual consulting, retention, change-in-control, fringe benefit, collective bargaining, bonus, incentive, deferred compensation, employee loan and all other employee benefit plans, agreements, programs, policies or other arrangements, whether or not subject to ERISA, whether formal or informal, oral or written.

FTAC Board means the board of directors of FTAC.

FTAC Charter means the second amended and restated certificate of incorporation of FTAC.

FTAC Class A Common Stock means the Class A common stock, par value $0.0001 per share, of FTAC.

FTAC Class B Common Stock means the Class B common stock, par value $0.0001 per share, of FTAC.

FTAC Class C Common Stock means the Class C common stock, par value $0.0001 per share, of FTAC to be authorized pursuant to the FTAC Charter.

FTAC Common Stock means FTAC Class A Common Stock and FTAC Class B Common Stock.

FTAC Contribution means, immediately following the Company LLC Contribution, the transfer by the LLC to the Accounting Predecessor, or a Subsidiary of the Accounting Predecessor, of all of the stock of FTAC, consummated prior to the consummation to the Additional I/C Loans.

FTAC Financing means the equity financing to be provided pursuant to the Forward Purchase Agreement.

FTAC Investors means certain entities affiliated with FTAC, including the Founder and Cannae LLC.

FTAC Organizational Documents means the FTAC Charter and FTACs bylaws, as amended and in effect on December 7, 2020.

FTAC Promissory Note means a promissory note issued on July 17, 2020 by FTAC to the Founder and an affiliate of the Founder, pursuant to which FTAC may borrow up to an aggregate principal amount of $800,000.

FTAC Public Shares means shares of FTAC Class A Common Stock sold as part of the units in the IPO (whether they are purchased in the IPO or thereafter in the open market).

6

Table of Contents

FTAC Public Stockholders means holders of the FTAC Public Shares, including the Founder and FTAC management team to the extent FTAC and/or members of FTAC management team purchase FTAC Public Shares, provided that Founders and each member of FTAC management teams status as a FTAC Public Stockholder will only exist with respect to such FTAC Public Shares.

FTAC Public Warrants means warrants included in the FTAC Units.

FTAC Schedules means the disclosure schedules of FTAC.

FTAC Stockholder Matters refers to (1) the adoption of the Merger Agreement and approval of the Transactions; (2) the amendment and restatement of the Certificate of Incorporation in the form of FTAC Charter attached as Annex B hereto; (3) the Omnibus Incentive Plan Proposal; and (4) any other proposals the Parties agree are necessary or desirable to consummate the Transactions.

FTAC Stockholder Redemption means providing FTACs stockholders with the opportunity to redeem shares of FTAC Class A Common Stock by tendering such shares for redemption not later than 5:00 p.m. Eastern Time on the date that is at least two (2) business days prior to the date of the Special Meeting.

FTAC Stockholders means the holders of shares of FTAC Common Stock.

FTAC Transaction Expenses means (i) the fees and disbursements of outside counsel to FTAC (including its direct and indirect equityholders), (ii) the fees and expenses of accountants to FTAC, (iii) the fees and expenses of the consultants and other advisors to FTAC set forth on Schedule 4.02(b)(i) of the FTAC Schedules, (iv) the fees and disbursements of bona fide third-party investment bankers and financial advisors to FTAC, (v) the placement fee set forth on Schedule 4.02(b)(ii) of the FTAC Schedules, and (vi) any premiums, fees, disbursements or expenses incurred in connection with any rep and warranty insurance policy and any tail insurance policy for the directors and officers liability insurance of FTAC, in each case, incurred in connection with the Transactions.

FTAC Units means the units sold in connection with FTACs IPO.

FTAC Working Capital Loans means loans the Founder or an affiliate of the Founder may, but are not obligated to, give the Company in order to finance transaction costs in connection with a Business Combination.

GAAP means generally accepted accounting principles in the United States.

GDPR means the EUs General Data Protection Regulation 2016/679, as amended.

Governance Proposal means the FTAC Stockholder vote, on a non-binding advisory basis, of certain governance provisions in the Company Bye-laws, presented separately in accordance with SEC guidance.

Governmental Authority means any federal, state, provincial, municipal, local or foreign government, governmental authority, regulatory or administrative agency, governmental commission, department, board, bureau, agency or instrumentality, court or tribunal.

Governmental Order means any order, judgment, injunction, decree, writ, stipulation, determination or award, in each case, entered by or with any Governmental Authority.

Group means, where appropriate, Paysafe and its subsidiaries.

HMRC means HM Revenue & Customs.

HSR Act means the Hart-Scott-Rodino Antitrust Improvements Act of 1976, as amended, and the rules and regulations promulgated thereunder.

7

Table of Contents

I/C Loans means the loans made by FTAC to the Company and the Accounting Predecessor out of the Available Cash Amount, made prior to the consummation of the Company LLC Contribution, FTAC Contribution and the Additional I/C Loans.

IPO means the initial public offering of FTAC Units, consummated on July 15, 2020.

IFRS means International Financial Reporting Standards as issued by the International Accounting Standards Board and adopted by the European Union.

Initial Business Combination means FTACs effecting of a merger, capital stock exchange, asset acquisition, stock purchase, reorganization or similar business combination with one or more businesses pursuant to the FTAC Charter.

Initial Founder Shares means all of the FTAC Class B Common Stock owned by the Founder and the independent directors on the board of directors of the Founder, which equals 36,675,836 shares of FTAC Class B Common Stock as of the date hereof and shall equal 28,687,959 shares of FTAC Class B Common Stock as of the Closing.

Initial Stockholders means the holders of Initial Founder Shares.

Insiders refers to William P. Foley, II, Richard N. Massey, Mark D. Linehan, Erika Meinhardt, David W. Ducommun, Michael L. Gravelle, C. Malcolm Holland and Bryan D. Coy.

Intended Tax Treatment means for U.S. federal income tax purposes (and for purposes of any applicable state or local income tax that follows U.S. federal income tax treatment), each of the Parties intention that (i) the Pubco Contribution should qualify as a transaction under Section 351 of the Code and should not subject shareholders of FTAC to tax under Section 367 of the Code (subject to entry into gain recognition agreements by any such shareholders required to enter into such agreements to preserve tax-free treatment under Section 367 of the Code), and (ii) the LLC Contribution should qualify as a transaction under Section 721 of the Code.

Intercreditor Agreement means that certain Intercreditor Agreement dated as of December 20, 2017, made between Paysafe Group Holdings II Limited (formerly Pi UK Holdco II Limited) as parent, Credit Suisse AG, London Branch as senior facility agent, Credit Suisse AG, London Branch as second lien facility agent, Credit Suisse AG, London Branch as security agent and the other Persons from time to time party thereto, as the same has been and may be further amended, restated, amended and restated, supplemented, replaced, refinanced, or otherwise modified from time to time in accordance with the terms thereof.

Lien means any mortgage, deed of trust, pledge, hypothecation, encumbrance, easement, license, option, right of first refusal, security interest or other lien of any kind.

LLC means, Paysafe Bermuda Holding LLC, a Bermuda exempted limited liability company.

LLC Contribution means, collectively, the Founder LLC Contribution and the Company LLC Contribution.

LLC Interests means the limited liability company interests in the LLC.

Merger means, immediately following the Founder LLC Contribution, on the terms and subject to the conditions of the Merger Agreement and in accordance with the DGCL and other applicable Laws, a business combination transaction by and among the Parties by which Merger Sub will merge with and into FTAC, with FTAC being the surviving corporation of the Merger, consummated prior to the consummation of the I/C Loans, the Company LLC Contribution, the FTAC Contribution and the Additional I/C Loans.

Merger Agreement means the agreement and plan of merger made and entered into as of December 7, 2020, by and among FTAC, the Company, Merger Sub, the LLC, the Accounting Predecessor and PGHL.

8

Table of Contents

Merger Sub means Paysafe Merger Sub Inc., a Delaware corporation and direct, wholly owned subsidiary of the Company.

No Redemption Scenario means no holder of FTAC Public Shares elects to have such shares redeemed in connection with the Business Combination.

Non-Founder FTAC Warrant means a FTAC Warrant, other than a Private Placement.

NYSE means the New York Stock Exchange.

OECD means the Organisation for Economic Co-operation and Development.

Omnibus Incentive Plan means the Paysafe Limited 2021 Omnibus Incentive Plan attached as Exhibit H to the Merger Agreement.

Omnibus Incentive Plan Proposal means the approval of the adoption of the Omnibus Incentive Plan.

Paysafe Audited 2019 Consolidated Financial Statements means the consolidated statement of financial position of Pi Jersey Holdco 1.5 Limited as of December 31, 2019, the related consolidated statements of comprehensive loss, shareholders equity, and cash flows, for the year ended December 31, 2019, and the related notes and comparative period for the year ended December 31, 2018.

Paysafe Consolidated Financial Statements means the Paysafe Audited 2019 Consolidated Financial Statements and the Paysafe Unaudited 2020 Interim Condensed Consolidated Financial Statements together.

Paysafe Contribution means, immediately following the PIPE Investment, PGHLs transfer and contribution of the Accounting Predecessor to the Company, in exchange for the Closing Seller Shares and the right to receive the Closing Cash Consideration, consummated prior to the consummation of the FTAC Financing, Founder FTAC Warrant Recapitalization, the Founder LLC Contribution, the Merger, the I/C Loans, the Company LLC Contribution, the FTAC Contribution and the Additional I/C Loans.

Paysafe Limited means Paysafe Limited, an exempted limited company incorporated under the laws of Bermuda.

Paysafe Parties means PGHL, the Accounting Predecessor, Merger Sub and the LLC.

Paysafe Unaudited 2020 Interim Condensed Consolidated Financial Statements means the unaudited condensed consolidated statement of financial position of Pi Jersey Holdco 1.5 Limited as of September 30, 2020, the related unaudited condensed consolidated statements of comprehensive loss, shareholders equity and cash flows for the nine-month periods ended September 30, 2020 and 2019, and the related notes.

PCAOB means the Public Company Accounting Oversight Board.

Permitted Acquisition means any acquisition of assets, equity interests or any business or other Person or division thereof by any Paysafe Party set forth on Schedule 1.01 of the PGHL Schedules, permitted under Section 7.01 of the Merger Agreement, or consented to by FTAC pursuant to Section 7.01(f) of the Merger Agreement.

PGHL means Paysafe Group Holdings Limited, a private limited company incorporated under the laws of England and Wales.

PGHL Benefit Plan has the meaning specified in Section 5.13(a) of the Merger Agreement.

9

Table of Contents

PGHL Employees means any current or former employee, officer, director or independent contractor of PGHL or its Subsidiaries.

PGHL Financing Agreements means the Senior Facilities Agreement, the Second Lien Facility Agreement, the Intercreditor Agreement, any L/C Facility Agreement, and the PPPSL Credit Agreement and each other Permitted Financing Document (as defined in the Intercreditor Agreement).

PGHL Schedules means the disclosure schedules of PGHL and its subsidiaries.

PGHL Transaction Expenses means (i) the fees and disbursements of outside counsel to PGHL (including its direct and indirect equityholders), (ii) the fees and expenses of accountants and other advisers to PGHL set forth on Schedule 4.02(a)(i) of the PGHL Schedules, (iii) the fees and disbursements of bona fide third-party investment bankers and financial advisors to PGHL, and (iv) any premiums, fees, disbursements or expenses incurred in connection with any tail insurance policy for the directors and officers liability insurance of PGHL, in each case, incurred in connection with the Transactions.

Pi Topco means Pi Jersey Topco Limited, a company incorporated in Jersey.

PIPE Investment means the commitments obtained by FTAC from certain investors for a private placement of Company Common Shares pursuant to those certain Subscription Agreements.

PIPE Investment Proceeds mean the aggregate amount funded and paid to the Company by the PIPE Investors pursuant to their Subscription Agreements.

PIPE Investor means an investor party to a Subscription Agreement.

POS means point of sale.

PPPSL Credit Agreement means that certain credit agreement dated as of June 18, 2019, among Paysafe Payment Processing Solutions LLC as borrower, the financial institutions from time to time party thereto as lenders, Woodforest National Bank, as administrative agent, and the other Persons from time to time party thereto, as the same has been and may be further amended, restated, amended and restated, supplemented, replaced, refinanced, or otherwise modified from time to time in accordance with the terms thereof.

Pre-Closing Recapitalization means the Company shall be permitted to adjust, split, combine, subdivide, recapitalize, reclassify or otherwise effect (including by merger) any change in respect of the then-outstanding Company Common Shares (including any such event that involves the creation of new classes of common shares of the Company, which may have varying voting rights on a per-share basis) as necessary or appropriate to facilitate the Transactions.

Principal Shareholders means, collectively, the Founder, Cannae LLC, the CVC Investors and the Blackstone Investors.

Private Placement Warrants means the Warrants sold to the Founder in a private placement in connection with the IPO.

Pubco Contribution means, collectively, the PIPE Investment, the Paysafe Contribution, and the Merger.

Record Date means the close of business on February 17, 2021.

Registration Rights Agreement means the agreement entered into by the Company, Pi Topco, PGHL, Cannae LLC, the Founder, the CVC Party and the Blackstone Investors in connection with the consummation of the Merger, attached to the Merger Agreement as Exhibit D.

Regulatory Consent Authorities means the Governmental Authorities with jurisdiction over enforcement of any applicable Law, including the FCA and the CBI.

10

Table of Contents

Schedules means the PGHL Schedules and the FTAC Schedules.

SEC Reports means all required registration statements, reports, schedules, forms, statements and other documents required to be filed by FTAC with the SEC since August 18, 2020.

Second Lien Facility Agreement means that certain Second Lien Facility Agreement dated as of December 20, 2017, among Paysafe Group Holdings II Limited (formerly Pi UK Holdco II Limited), Paysafe Group Holdings III Limited (formerly Pi UK Holdco III Limited), the Persons from time to time party thereto as Borrowers and as Guarantors (in each case, as defined therein), the financial institutions from time to time party thereto as lenders, Credit Suisse AG, London Branch, as agent and as security agent, and the other Persons from time to time party thereto, as the same has been and may be further amended, restated, amended and restated, supplemented, replaced, refinanced, or otherwise modified from time to time in accordance with the terms thereof.

Senior Facilities Agreement means that certain Senior Facilities Agreement dated as of December 20, 2017, among Paysafe Group Holdings II Limited (formerly Pi UK Holdco II Limited), Paysafe Group Holdings III Limited (formerly Pi UK Holdco III Limited), the Persons from time to time party thereto as TLB Borrowers, RCF Borrowers, and as Guarantors (in each case, as defined therein), the financial institutions from time to time party thereto as lenders, Credit Suisse AG, London Branch, as agent and as security agent, and the other Persons from time to time party thereto, as the same has been and may be further amended, restated, amended and restated, supplemented, replaced, refinanced, or otherwise modified from time to time in accordance with the terms thereof.

Shareholders Agreement means the agreement entered into by the Company, Pi Topco, PGHL and the Principal Shareholders in connection with the consummation of the Merger, attached to the Merger Agreement as Exhibit D.

SMB means small and medium-sized businesses.

Special Meeting means a meeting of the holders of FTAC Common Stock to be held for the purpose of approving the FTAC Stockholder Matters.

Specified Net Debt Amount means $1,805,000,000.

Sponsor Agreement means that certain Amended and Restated Letter Agreement, dated as of December 7, 2020, by and among the Founder, FTAC, the Company and certain other parties thereto, as amended, restated, modified or supplemented from time to time.

Sponsor Person has the meaning specified in the Sponsor Agreement.

Subscription Agreement means each individual subscription agreement entered into by each PIPE Investor.

Termination Date means December 7, 2021.

Transaction Agreements means the Merger Agreement, the Registration Rights Agreement, the Shareholders Agreement, the Sponsor Agreement, the Forward Purchase Agreement, the Subscription Agreements, the Company Charter, the Company Bye-laws, the FTAC Charter, and all the agreements, documents, instruments and certificates entered into in connection herewith or therewith and any and all exhibits and schedules thereto.

Transaction Expenses means the aggregate amount of the PGHL Transaction Expenses and FTAC Transaction Expenses.

11

Table of Contents

Transactions means the transactions contemplated by the Merger Agreement, including the Merger, the Paysafe Contribution, the FTAC Contribution, the Founder LLC Contribution, the Company LLC Contribution and the Pre-Closing Recapitalization.

Trasimene Capital means Trasimene Capital Management, LLC, a financial advisory firm led by William P. Foley, II.

Treasury Regulations means the regulations, including proposed and temporary regulations, promulgated under the Code.

Trust Account has the meaning specified in Section 6.07(a) of the Merger Agreement.

Trust Agreement means the Investment Management Trust Agreement, dated August 21, 2020, by and between FTAC and the Trustee on file with the SEC Reports of FTAC as of December 7, 2020.

Trustee means Continental Stock Transfer & Trust Company, a New York corporation.

U.S. dollar, USD, US$ and $ mean the legal currency of the United States.

VAT means any: (a) tax imposed in compliance with the council directive of 28 November 2006 on the common system of value added tax (EC Directive 2006/112) (including, in relation to the UK, value added tax imposed by the Value Added Tax Act 1994 and legislation and regulations supplemental thereto); and (b) other tax of a similar nature (including, without limitation, sales tax, use tax, consumption tax and goods and services tax), whether imposed in a member state of the European Union in substitution for, or levied in addition to, such tax referred to in (a), or elsewhere.

VWAP means, for any security as of any date(s), the dollar volume-weighted average price for such security on the principal securities exchange or securities market on which such security is then traded during the period beginning at 9:30:01 a.m., New York time, and ending at 4:00:00 p.m., New York time, as reported by Refinitiv Workspace or, if the foregoing does not apply, the dollar volume-weighted average price of such security in the over-the-counter market on the electronic bulletin board for such security during the period beginning at 9:30:01 a.m., New York time, and ending at 4:00:00 p.m., New York time, as reported by Refinitiv Workspace, or, if no dollar volume-weighted average price is reported for such security by Refinitiv Workspace for such hours, the average of the highest closing bid price and the lowest closing ask price of any of the market makers for such security as reported by OTC Markets Group Inc.

Warrant Agreement means that certain Warrant Agreement, dated as of August 21, 2020, between FTAC and Continental Stock Transfer & Trust Company, a New York corporation.

12

Table of Contents

QUESTIONS AND ANSWERS ABOUT THE PROPOSALS

| Q. Why am I receiving this proxy statement/ prospectus? | A. FTAC, PGHL, the Company, Merger Sub, the Accounting Predecessor and the LLC (PGHL, the Accounting Predecessor, Merger Sub and the LLC, together, the Paysafe Parties) have agreed to the Business Combination under the terms of the Merger Agreement that is described in this proxy statement/prospectus and is attached to this proxy statement/prospectus as Annex A. The Merger Agreement provides that, among other things, (i) Merger Sub will merge with and into FTAC, with FTAC being the surviving corporation in the merger and an indirect subsidiary of the Company and each outstanding share of FTAC Class A Common Stock and FTAC Class B Common Stock (other than certain excluded shares) will convert into the right to receive one Company Common Share, and (ii) PGHL will transfer and contribute the Accounting Predecessor to the Company in exchange for Company Common Shares and cash.

This proxy statement/prospectus and its annexes contain important information about the proposed Business Combination and the other matters to be acted upon at the Special Meeting. You should read this proxy statement/prospectus and its annexes carefully and in their entirety. See the section entitled Proposal No. 1The Business Combination Proposal. |

|

| Q. When and where is the Special Meeting? | A. The Special Meeting will be held on March 25, 2021, at 12:00 p.m., Eastern Time via live webcast at https://www.cstproxy.com/foleytrasimene2/sm2021. | |

| Q. Can I attend the Special Meeting in person? | A. No. You will not be able to attend the Special Meeting in person. FTAC will be hosting the Special Meeting via live webcast on the Internet. The webcast will start at 12:00 p.m. Eastern Time, on March 25, 2021. Any stockholder can listen to and participate in the Special Meeting live via the Internet at https://www.cstproxy.com/foleytrasimene2/sm2021. You will be able to attend the Special Meeting online and vote during the Special Meeting by visiting https://www.cstproxy.com/foleytrasimene2/sm2021. | |

| Q. What do I need in order to participate in the Special Meeting online? | A. You can attend the Special Meeting via the Internet by visiting https://www.cstproxy.com/foleytrasimene2/sm2021. | |

| Q. What is being voted on at the Special Meeting? | A. FTACs stockholders are being asked to consider and vote upon a proposal to approve the Business Combination described in the accompanying proxy statement/prospectus, including (a) adopting the Merger Agreement, (b) approving the issuance of the Class C Common Stock in exchange for the warrants held by the FTAC Founder and (c) approving the other transactions contemplated by the Merger Agreement and related agreements described in the accompanying proxy statement/prospectus. See the section entitled Proposal No. 1The Business Combination Proposal. | |

| FTACs stockholders are also being asked to consider and vote upon a proposal to approve and adopt the third amended and restated certificate of incorporation of FTAC. See the section entitled Proposal No. 2The Charter Amendment Proposal.

FTACs stockholders are also being asked to consider and vote upon, on a non-binding advisory basis, certain governance provisions in the Company Bye-laws, presented separately in accordance with the SEC requirements. See the section entitled Proposal No. 3The Governance Proposal. |

||

13

Table of Contents

| FTACs stockholders are also being asked to consider and vote on a proposal to approve and adopt the Paysafe Limited 2021 Omnibus Incentive Plan and the material terms thereunder, including the authorization of the initial share reserve thereunder. See the section entitled Proposal No. 4The Omnibus Incentive Plan Proposal.

FTACs stockholders may also be asked to consider and vote upon an Adjournment Proposal, which is a proposal to adjourn the Special Meeting to a later date or dates to permit further solicitation and voting of proxies if, based upon the tabulated vote at the time of the Special Meeting, FTAC would not have been authorized to consummate the Business Combination. See the section entitled Proposal No. 5The Adjournment Proposal. |

||

| FTAC will hold the Special Meeting of its stockholders to consider and vote upon these proposals. This proxy statement/prospectus contains important information about the proposed Business Combination and the other matters to be acted upon at the Special Meeting. Stockholders should read it carefully. | ||

| Q. Are the proposals conditioned on one another? | A. Unless the Business Combination Proposal is approved, the Omnibus Incentive Plan Proposal and Charter Amendment Proposals will not be presented to the FTAC Stockholders at the Special Meeting. The Adjournment Proposal is not conditioned on the approval of any other proposal set forth in this proxy statement/prospectus. It is important for you to note that in the event that the Business Combination Proposal does not receive the requisite vote for approval, then FTAC will not consummate the Business Combination. In addition, if the Charter Amendment Proposal does not receive the requisite vote for approval, then FTAC will not consummate the Business Combination. If FTAC does not consummate the Business Combination and fails to complete an initial business combination by August 21, 2022 (or such later date as FTAC Stockholders may approve in accordance with its Current Charter), FTAC will be required to dissolve and liquidate the Trust Account by returning the then remaining funds in such account to its public stockholders. | |

| The vote of stockholders is important. Stockholders are encouraged to submit their completed proxy card as soon as possible after carefully reviewing this proxy statement/prospectus. | ||

| Q. Why is FTAC proposing the Business Combination? | A. FTAC was organized to effect a merger, capital stock exchange, asset acquisition, stock purchase, reorganization or similar business combination with one or more businesses. | |

| FTAC completed its initial public offering (the IPO) of Units on August 21, 2020, with each Unit consisting of one share of its FTAC Class A Common Stock and one-third of one FTAC Warrant. Each whole FTAC Warrant entitles the holder to purchase one share of FTAC Class A Common Stock at a price of $11.50. FTAC also closed on the sale of the Units subject to over-allotment on August 21, 2020, raising total gross proceeds of $1,300,000,000. On August 26, 2020, the underwriters partially exercised their over-allotment option, resulting in an additional 16,703,345 Units issued for an aggregate amount of $167,033,450. In connection with the underwriters partial exercise of their over-allotment option, FTAC also consummated the sale of an additional 2,227,113 Private Placement Warrants at $1.50 per Private Placement Warrant, generating total proceeds of $3,340,669. A total of $167,033,450 was deposited into the Trust Account, bringing the total Units sold in the IPO to 146,703,345 Units and the aggregate proceeds held in the Trust Account as of such date to $1,467,033,450. | ||

14

Table of Contents

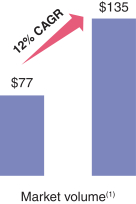

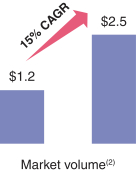

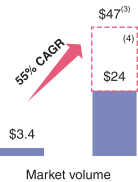

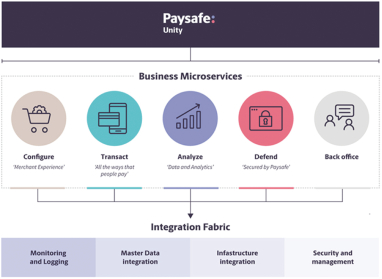

| Paysafe is a leading, global pioneer in digital commerce with over $98 billion in volume processed in 2019 and $73 billion processed for the nine months ended September 30, 2020. Paysafe generated $1.4 billion in revenue in 2019 and $1.1 billion in revenue for the nine months ended September 30, 2020, with net losses of $110 million and $116 million during the same periods, respectively. Paysafe empowers over 15 million active users in more than 120 countries and over 250,000 small and medium businesses (SMBs) across the United States, Canada and Europe to conduct secure and friction-less commerce across online, mobile, in-app and in-store channels, generating over 75% of its revenue from eCommerce and Integrated Commerce solutions. Paysafe focuses on specialized and high-risk industry verticals, including iGaming (which encompasses a broad selection of online betting related to sports, esports, fantasy sports, poker and other casino games), digital trading, cryptocurrencies, nutraceuticals, Cannabidiol (CBD) products and multi-level marketing, which represented approximately $640 million, or 45%, of its revenue for the year ended December 31, 2019. | ||

| After careful consideration, the FTAC Board has determined that the Business Combination Proposal, the Charter Amendment Proposal, the Governance Proposal, the Omnibus Incentive Plan Proposal and the Adjournment Proposal are fair to and in the best interests of FTAC and its stockholders and recommends voting FOR the Business Combination Proposal, FOR the Charter Amendment Proposal, FOR the Governance Proposal, FOR the Omnibus Incentive Plan Proposal and, if presented, FOR the Adjournment Proposal. See Proposal No. 1The Business CombinationFTACs Board of Directors Reasons for Approval of the Business Combination for additional information. Consummation of the Transactions is conditioned on the approval of each of the Business Combination Proposal and the Charter Amendment Proposal. If either of those proposals are not approved, we will not consummate the Transaction. | ||

| Q. What will happen in the Business Combination? | A. At the Closing, Merger Sub will merge with and into FTAC, with FTAC surviving such Merger. Upon consummation of the Merger, FTAC will become a wholly-owned indirect subsidiary of the Company and holders of FTAC securities will exchange their FTAC securities for securities of the Company. In particular, among other transactions, (i) each outstanding share of FTAC Class A Common Stock (excluding shares that are redeemed by the holders) and each outstanding share of FTAC Class B Common Stock (28,687,959 shares following the Founders forfeiture to FTAC for cancellation of 7,987,877 Founder Shares) will be converted into one Company Common Share, and (ii) each outstanding FTAC Warrant (other than Private Placement Warrants) will become one Company Warrant that will entitle the holder thereof to purchase one Company Common Share in lieu of one share of FTAC Class A Common Stock. | |

| Q. What equity stake will current stockholders of FTAC, the PIPE Investors, and PGHL hold in the post-combination company after the closing? | A. Upon consummation of the Business Combination, the Company will become a new public company and FTAC will become a wholly-owned subsidiary of the Company. PGHL, the former security holders of FTAC, and the PIPE Investors will all become security holders of the Company. See the section entitled Beneficial Ownership of Securities.

It is anticipated that, upon completion of the Business Combination: (i) FTACs public stockholders (excluding Cannae) will hold approximately 20.4% of the outstanding common shares of the post-combination company; (ii) the PIPE Investors (excluding Cannae) will hold approximately 22.9% of the outstanding common |

|

15

Table of Contents

| shares of the post-combination company; (iii) Cannae (excluding amounts included in Founder) will hold approximately 7.0% of the outstanding common shares of the post-combination company; (iv) the Founder (including Cannae) will hold approximately 4.0% of the outstanding common shares of the post-combination company; and (v) PGHL, which will be jointly controlled by the CVC Investors and the Blackstone Investors, will hold approximately 45.7% of the outstanding common shares of the post-combination company. These levels of ownership interest: (i) exclude the impact of the shares of FTAC Class A Common Stock underlying the FTAC Warrants and (ii) assume the No Redemption Scenario.

For more information, please see the sections entitled Beneficial Ownership of Securities, and Unaudited Pro Forma Condensed Combined Financial Information. |

||